By Samuel Bell in Rhode Island's Future

But individual

consumers form the heart of our economy. We are the ones who power

growth, and when numbers move in the behemoth that is the household sector, the

consequences can be massive.

That is why the

explosion in Rhode Island household debt in 2015 is so important.

Every year, the New

York Fed tracks per capita state household debt, publishing numbers for the

fourth quarter of every year.

Their new numbers contain shocking news for our state.

While per capita household debt went up by $290 nationally from 2014Q4 to

2015Q4, it exploded by $1,240 in Rhode Island.

Statewide, we’re

talking about $1.09 billion.*

To put that number in

context, it is a bit bigger than the sales tax. It is 2.1 percent of

our state’s personal income. It is so huge that it swamps the effect of just

about every 2014 economic policy.

State policy has a

very important effect on economic outcomes, but large swings in household debt

can sometimes drive enormous changes in the economy.

If taxpayers go deep into debt, it can more than compensate for bad state policy. For instance, Jeb Bush presided over a surging Florida economy mainly because his term corresponded to a catastrophic spike in household debt fueled by a gargantuan housing bubble.** But when the music stopped, Floridians were mired in debt, and the state economy cratered.

That’s why it’s

important to watch household debt levels closely. If ordinary consumers are

going into debt, it can mask the effect of bad public policy.

In 2015, Rhode

Island’s economic performance was fairly mediocre. Per capita income rose by

3.6 percent, compared to a nationwide average of 3.5 percent. But if you

take the debt numbers into consideration, you’d normally expect very strong

growth. Basically, it looks an awful lot like Rhode Islanders dipped into our

personal finances to bail out bad policy.

*The New York Fed only

surveys people with a credit report and a social security card. We don’t

really know what’s going on in the rest of the population.

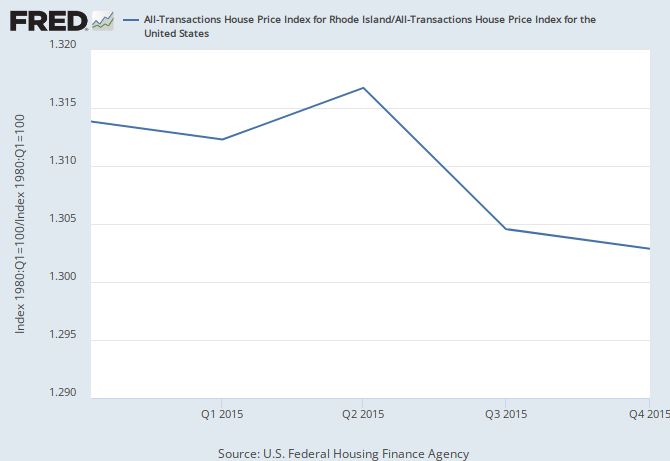

**In Rhode Island, the

debt surge can’t be explained by a sudden housing bubble. In fact, Rhode

Island house prices fell a tiny bit relative to the US average.

{kind=link}

Samuel Bell is the Rhode Island State Coordinator for the Progressive

Democrats of America. My primary interest is Rhode Island's economy and what we

can do to fix it.