Trump’s Economic Team Is a Who’s Who of What’s Wrong

By Richard Eskow for the Campaign for America's Future Blog

“I hear America singing,” Walt Whitman

wrote, “the varied carols I hear.” Donald Trump hears America singing, too. But

where Whitman heard men and women, masons and carpenters, Trump hears only the

unvarying monotone of rich white males like himself.

“I hear America singing,” Walt Whitman

wrote, “the varied carols I hear.” Donald Trump hears America singing, too. But

where Whitman heard men and women, masons and carpenters, Trump hears only the

unvarying monotone of rich white males like himself.

Trump’s

tone-deafness was in full effect last week, when he announced his team of economic

advisers in

advance of what is being billed as “a major economic address” in Detroit on

Monday.

Trump’s team

isn’t just monochromatic and male. At least four, and perhaps as many six, of

the men are billionaires.

They range in age from 50 to 74 – or, from “younger old white guy” to “older

old white guy.”

Five team

members are named Steve – which means that eight of them are not. For

diversity, that will have to do.

There are only

two economists on the team – and one of them believes in the flat tax.

But hedge funds

are represented. So is fracking. And tobacco. And guns. And banking. And steel.

And there’s the guy who mismanaged Chrysler before it was rescued by a

government intervention.

Three team

members – economist Peter Navarro, steel magnate Dan DiMicco and real estate

investor Thomas Barrack Jr. – have criticized the bad “trade” deals supported

by both major parties over the last 25 years. That’s a start, I suppose. But

it’s not enough, not by a long shot.

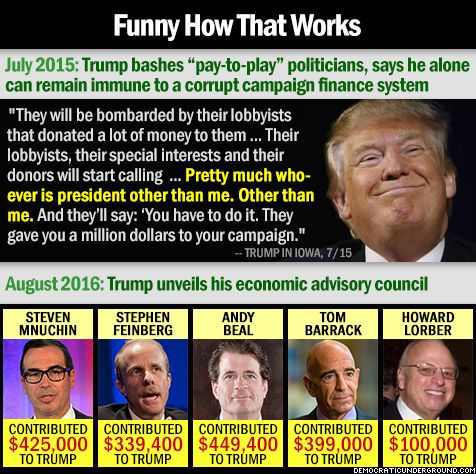

(As for Barrack,

he says he raised $32

million for a Trump super PAC from only four donors. He also hosted a

Trump fundraiser for $25,000 a ticket – or $100,000 per couple. So much for

“the candidate who can’t be bought because he doesn’t need the money.”)

Who’s not

represented on Trump’s economic team? Working people. Women. Minorities. The

middle class.

There are no

union leaders or labor economists to explain why higher wages and a more

unionized workforce leads to broader growth prosperity. There’s nobody who’s

fighting to close the gender pay gap, or to resist the economic predation that

has decimated minority communities.

There’s no one who understands the

devastating impact that environmental destruction is having on our economy, as

well as on our planet and on our bodies.

So who are these

men? Old caper movies introduce their players with a montage of them living

their daily lives. Here, then, is the Trump Team montage:

Andrew

Beal, banker: Beal made his

billions buying up distressed properties, sometimes from government agencies.

He reportedly plays rough at collection time. “Mr. Beal acknowledges that some

debt collectors engaged by his banks may have pushed too hard,” the Wall Street Journal wrote.

Beal likes to

play high-stakes poker. He is known for offering risky loans –

and because he owns a bank, the US government insures them.

Speaking of

government, we forgot to mention: this federally insured tycoon is a

libertarian.

Steve

Feinberg, financier: Feinberg runs Cerberus Capital

Management, which bought Chrysler in 2007 with some other investors

and promised to restore it to profitability. Instead they declared bankruptcy

and accepted federal bailout money for Chrysler Financial.

Cerberus also

purchased a majority share of GMAC in 2006 and accepted federal bailout money

for it, too (after the Fed bent the rules and declared it a bank holding

company).

Then there are

the guns. Cerberus purchased Bushmaster Firearms International, Remington Arms,

and several other firearms companies, and merged them all into an entity called

the “Freedom Group.”

It took an investor revolt to make Cerberus promise to

unload these holdings after Bushmaster’s AR-15 was used to kill a number of

small children in the Sandy Hook shootings. (It later reneged, saying

it couldn’t find a buyer.)

Cerberus also

promised to stay out of the gun debate, but two years after Sandy Hook its

executives were funding anti-gun

control ads – in Connecticut, where the kindergarten massacre

occurred.

Feinberg is a major Republican

donor. He now says he regrets naming his firm for the three-headed

dog that guards the gates of hell.

Steven

Mnuchin, financier/film producer: Mnuchin’s investment group “bailed out” a housing

lender in California and renamed it OneWest. OneWest, where Mnuchin became CEO,

has been strongly criticized for its foreclosure practices.

The California

Reinvestment Coalition has called on authorities to

investigate OneWest’s apparent pattern of racial discrimination in

foreclosures. It also cited its abusive “foreclosures of widows,” which makes

it morally indistinguishable from countless silent-movie villains.

On the plus

side, Mnuchin was an executive producer on “Mad Max: Fury Road.”

Harold

Hamm, Oklahoma oil billionaire: Hamm is, among other things, a fracker with

extensive holdings in the Bakken Formation.

Bloomberg News reports

that Hamm attempted to have some earthquake researchers fired from the

University of Oklahoma, where he’s a major donor, because they were

investigating the connection between the oil and gas industry and Oklahoma’s

“nearly 400-fold increase in earthquakes.”

Hamm, who is reportedly worth $11.3 billion, was cited as one

of the executives urging Mitt Romney to turn federal lands over to states for

oil and gas exploitation.

Believe it or

not, this fracker is reportedly under consideration for the job of Energy Secretary in

a Trump Administration.

John

Paulson, hedge funder: Paulson made

billions using credit default swaps to bet against subprime mortgages in the

run-up to the 2008 financial crisis. That’s no crime, and Paulson guessed right

– although it did lead to labels like “the hedge funder who

bet against America.”

Paulson’s

actions reinforce the idea that today’s hedge funds are economically harmful

entities. It’s fine for an airline to hedge against the price of oil to protect

its bottom line. But it’s hard to see how the bets made by today’s hedge funds

help the economy. They are destructive when they lead to market manipulation or

the entrapment of unwary investors.

Speaking of

which: Paulson went to Goldman Sachs in 2006 and said he wanted to bet against

subprime mortgages. Goldman needed a buyer for those investments, which were

then packaged as a “collateralized debt obligation” or “CDO” called “Abacus.”

It did not reveal that Paulson had shorted them by more than $1 billion.

(Summaries here and here.)

Goldman Sachs

paid more than half a

billion dollars ($550 million) to settle the case.

Paulson, who was not accused of wrongdoing, made about $1 billion on the deal.

(He’s fallen on harder times lately,

although presumably not the “foreclosed widow” kind of hard times.)

“Some investors

later would argue that Mr. Paulson’s actions indirectly led to the creation of

additional dangerous CDO investments,” The Wall Street Journal reported, “resulting

in billions of dollars of additional losses for those who owned the CDO

slices.”

That’s a

sensible interpretation. Meanwhile, Americans were left wondering what this

kind of activity does for them or the economy as a whole – or why their

economic future should be entrusted to someone with this sort of background.

These are the

architects of the economy Trump would create: a fracker for Energy Secretary,

harmful speculators in key advisory roles, and an economy controlled by people

who foreclose on widows and profit from gun violence.

The America

Trump describes is a dark dystopia, competitive and divided and brutal. Now

he’s assembled a team that could make that nightmare a reality. We thought

“Fury Road” was just a movie. Who knew it was a presidential platform, too?

Richard (RJ) Eskow is a senior fellow

at Campaign for America's Future.