Have

Voters Killed the Crappy Coverage Comeback?

Democrats

seized the House while Republicans increased their majority in the Senate, but

the unambiguous and across-the-board winner in the election was regulation –

specifically, regulation of the health insurance industry.

Democrats

seized the House while Republicans increased their majority in the Senate, but

the unambiguous and across-the-board winner in the election was regulation –

specifically, regulation of the health insurance industry.

Rarely

has the public sent such a clear message that it wanted government to rein in

corporations and market forces in favor of consumer and public interest

protections.

The desire to retain provisions of the Affordable Care Act protecting those with pre-existing conditions was key to Democratic gains. Republicans responded by pretending they agreed with that principle, but few were fooled by this deception.

The desire to retain provisions of the Affordable Care Act protecting those with pre-existing conditions was key to Democratic gains. Republicans responded by pretending they agreed with that principle, but few were fooled by this deception.

At

the same time, voters in three deep red states – Idaho, Nebraska and Utah –

approved ballot initiatives in favor of ACA Medicaid expansion. This amounted

to an embrace not just of regulation but of out-and-out government-controlled

health coverage.

All these results should put an end to the longstanding Republican crusade to repeal the ACA, but it remains to be seen whether there is also a termination of the Trump Administration’s effort to undermine the law through steps such as allowing wider sale of substandard policies.

One

encouraging sign came even before the votes were counted. On November 2 a

federal judge in Miami, acting at the request of the Federal Trade

Commission, issued an order temporarily shutting down a Florida company called

Simple Health Plans LLC, which along with related firms was selling policies

the FTC called “predatory” and “worthless.”

The

FTC complaint against the companies spells

out a variety of deceptive practices meant to make customers think they were

buying real coverage when in fact they were getting medical discount

memberships of limited value.

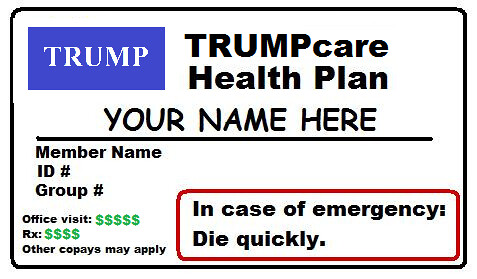

It’s

telling that one of the websites used by the firms is called

Trumpcarequotes.com. Trumpcare is actually an appropriate term for the crappy

coverage—both because Trump has been touting such plans and because the Trump

name has been involved in previous scams such as Trump University.

Let’s not forget that after his election Trump had to pay $25 million to settle litigation related to that venture, a step that the New York State Attorney General called“a major victory for the over 6,000 victims of his fraudulent university.”

Let’s not forget that after his election Trump had to pay $25 million to settle litigation related to that venture, a step that the New York State Attorney General called“a major victory for the over 6,000 victims of his fraudulent university.”

The

ACA’s provisions relating to protection for pre-existing conditions are

inseparable from those setting minimum standards for coverage. Ensuring the

right of patients to buy insurance is meaningless if they end up with plans

that pay for next to nothing.

The

proliferation of junk insurance through the efforts of companies such as Aetna

was one of the dismal realities of the U.S. health insurance market that gave

rise to the ACA.

Republicans have been promoting similar low-cost plans as their solution to the supposed crisis of Obamacare.

This is a cynical ploy to use a perverse form of consumerism to restore the old days of limited regulation. Let’s hope the election results have taught them a lesson about the consequences of messing with healthcare.

Republicans have been promoting similar low-cost plans as their solution to the supposed crisis of Obamacare.

This is a cynical ploy to use a perverse form of consumerism to restore the old days of limited regulation. Let’s hope the election results have taught them a lesson about the consequences of messing with healthcare.