Mainstream economics doesn't agree on WHY inflation is happening and doesn't have any solutions

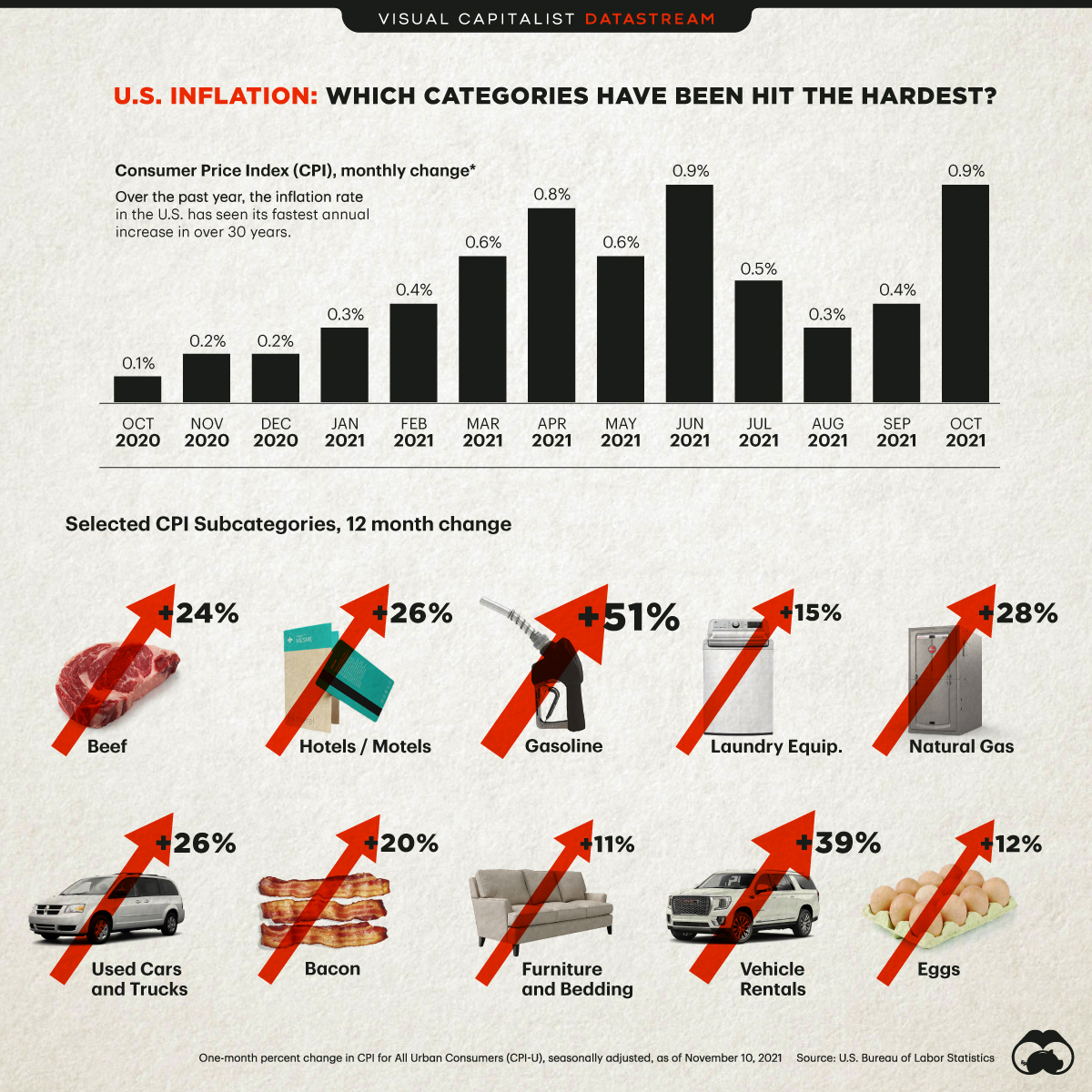

Since 2021, prices have surged dramatically across countries and inflation has become a global challenge. Global central banks delivered historic rate hikes in 2022 in order to tame inflation and continued doing so even when inflation was falling, thereby risking a global recession.

Indeed, for the past five months, average inflation in the U.S. has been at 2.4%. Across Europe, inflation has also been dropping. In Spain, for instance, consumer prices rose 5.8% in December, down from 6.8% in the previous month. The December figure represented the fifth consecutive month of declining inflation in Spain.

Yet, the European Central Bank—which like the U.S. Federal Reserve has also set the target rate for inflation at the arbitrary number of 2% per year—plans to continue raising interest rates “significantly further” as it deems that inflation “remains far too high and is projected to stay above the target for too long.”

Meanwhile, both the U.S. and European economies are expected to enter a recession in 2023. For what it’s worth, the head of the IMF expects a full one-third of the world to slide into recession this year.

What has been causing the upward trends in inflation and why do central banks around the world keep raising interest rates, a policy which will slow economic growth and result in lower wage increases and fewer jobs?

What has been causing the upward trends in inflation and why do central banks around the world keep raising interest rates, a policy which will slow economic growth and result in lower wage increases and fewer jobs?

Several factors are at play in causing a surge in prices, which include the Covid-19 pandemic, geopolitics, and corporate mark-ups and profit margins, while pure capitalist logic and interests explain why central banks are raising interest rates to fight inflation.

These were some of the conclusions reached by the progressive economists who participated in an international conference on “Global Inflation Today” organized by the renowned Political Economy Research Institute (PERI) at the University of Massachusetts Amherst and held from December 2-3, 2022.

To start with, a co-authored paper by Robert Pollin (Distinguished Professor of Economics and Co-Director of PERI at UMass Amherst) and Hanae Bouazza shows convincingly that there is no justification why the Federal Reserve and other central banks aim for an inflation target of 2%.

These were some of the conclusions reached by the progressive economists who participated in an international conference on “Global Inflation Today” organized by the renowned Political Economy Research Institute (PERI) at the University of Massachusetts Amherst and held from December 2-3, 2022.

To start with, a co-authored paper by Robert Pollin (Distinguished Professor of Economics and Co-Director of PERI at UMass Amherst) and Hanae Bouazza shows convincingly that there is no justification why the Federal Reserve and other central banks aim for an inflation target of 2%.

Indeed, their research finds “no consistent evidence supporting the conclusion that economies at any income level will achieve significant GDP benefit when they maintain inflation within low single digits, i.e., between the 0 – 2.5 percent inflation range.”

Not only that, but the “evidence… suggests that, in general, economies are more likely to achieve higher GDP growth rates in association with inflation ranges in the range of 2.5 – 5 percent, 5 – 10 percent and, for the most part, 10 – 15 percent.”

These are significant findings which raise serious questions about the goals of macro policy. Indeed, if inflation-targeting policy is not conducive to promoting economic growth, what is its primary aim?

These are significant findings which raise serious questions about the goals of macro policy. Indeed, if inflation-targeting policy is not conducive to promoting economic growth, what is its primary aim?

Citing the work of scholars who have done extensive research around this question, such as Gerald Epstein (Professor of Economics and Co-Director of PERI at UMass Amherst) and others, Pollin and Bouazza suggest that corporate profitability is the primary aim of inflation-targeting policy.

“Protecting the wealth of the wealthy” is the reason why the Fed has taken aggressive steps to tame inflation by raising interest rates, Epstein pointed out in a recent joint interview with Pollin.

Needless to say, the mainstream economic paradigm keeps silent on such matters, and one will never find answers in it on the most important processes that affect the workings of the real world and on the issues that are of paramount importance to the lives of working people.

To be sure, mainstream economics failed miserably in addressing the financial crisis of 2007-08, so why would it be any different now when it comes to making sense of the rising inflation of the past 18 months?

With regard to the actual causes of inflation in 2021-22, a paper co-authored by Asha Banerjee and Josh Bivens of the Economic Policy Institute identifies the Covid-19 pandemic and the Russian invasion of Ukraine as key factors in the inflationary surge of the past 18 months or so but argues that profit mark-ups added immensely to inflationary pressures over the same period.

Needless to say, the mainstream economic paradigm keeps silent on such matters, and one will never find answers in it on the most important processes that affect the workings of the real world and on the issues that are of paramount importance to the lives of working people.

To be sure, mainstream economics failed miserably in addressing the financial crisis of 2007-08, so why would it be any different now when it comes to making sense of the rising inflation of the past 18 months?

With regard to the actual causes of inflation in 2021-22, a paper co-authored by Asha Banerjee and Josh Bivens of the Economic Policy Institute identifies the Covid-19 pandemic and the Russian invasion of Ukraine as key factors in the inflationary surge of the past 18 months or so but argues that profit mark-ups added immensely to inflationary pressures over the same period.

Of equal importance here is that the authors present more than sufficient evidence to counter the mainstream economic perspective that lays the blame for the rise of inflation in the U.S. on the American Rescue Plan. Indeed, the data they present, on both the domestic and international fronts, does not support the claim that too much fiscal spending overheated the economies, fueling runaway inflation.

Another paper presented at the PERI conference, co-authored by C. P. Chandrasekhar and Jayati Ghosh, on how low-and middle-income countries can respond to inflation, also argues that there are more important factors than the pandemic and Russia’s invasion of Ukraine behind the current inflation crisis.

Another paper presented at the PERI conference, co-authored by C. P. Chandrasekhar and Jayati Ghosh, on how low-and middle-income countries can respond to inflation, also argues that there are more important factors than the pandemic and Russia’s invasion of Ukraine behind the current inflation crisis.

The sharp rise in global prices of food and fuel, Chandrasekhar and Ghosh contend, was driven by “profiteering, price expectations, and associated speculation.” They show, for instance, that while there were sharp spikes in the prices of food and fuel between February and July 2022, “the supplies of oil and gas to Europe remained largely unaffected.”

The analyses on inflation and its causes, as well as the actual aims of inflation-targeting policy, made by all of the presenters at the PERI conference (which included many leading progressive economists such as William Spriggs, Gerald Epstein, Thomas Ferguson, Nancy Folbre, James K. Galbraith, Servaas Storm, and Isabella Weber, among others) can be described as a Progressive Political Economy Guide to Inflation.

The analyses on inflation and its causes, as well as the actual aims of inflation-targeting policy, made by all of the presenters at the PERI conference (which included many leading progressive economists such as William Spriggs, Gerald Epstein, Thomas Ferguson, Nancy Folbre, James K. Galbraith, Servaas Storm, and Isabella Weber, among others) can be described as a Progressive Political Economy Guide to Inflation.

Indeed, they show how powerful heterodox economic approaches are in disclosing the real forces driving inflation and the actual reasons for central banks raising sharply interest rates. And, by extension, they also reveal the flaws and limitations of mainstream economics, which is in dire need of a major overhaul.

C.J. POLYCHRONIOU is a political economist/political scientist who has taught and worked in numerous universities and research centers

C.J. POLYCHRONIOU is a political economist/political scientist who has taught and worked in numerous universities and research centers