Eli Lilly is cutting insulin prices and capping copays at $35

Dana Goldman, University of Southern California and Karen Van Nuys, University of Southern California

Pharmaceutical giant Eli Lilly is slashing the list prices for some of its most popular insulin products by 70% and capping insulin copays at US$35 for uninsured patients and those with private health insurance. These changes follow efforts by the federal government, the California state government, nonprofits and some companies to make insulin more affordable for the more than 7 million Americans with diabetes who require it.

High prices (and profits) in the US finally became an

embarrassment for Big Pharma

The Conversation asked Dana Goldman and Karen Van Nuys, two scholars who have researched insulin pricing, to explain why Eli Lilly is dramatically cutting the cost of some of its insulin products and to sum up how it may improve access to this essential medical treatment.

1. Why is Lilly reducing prices now?

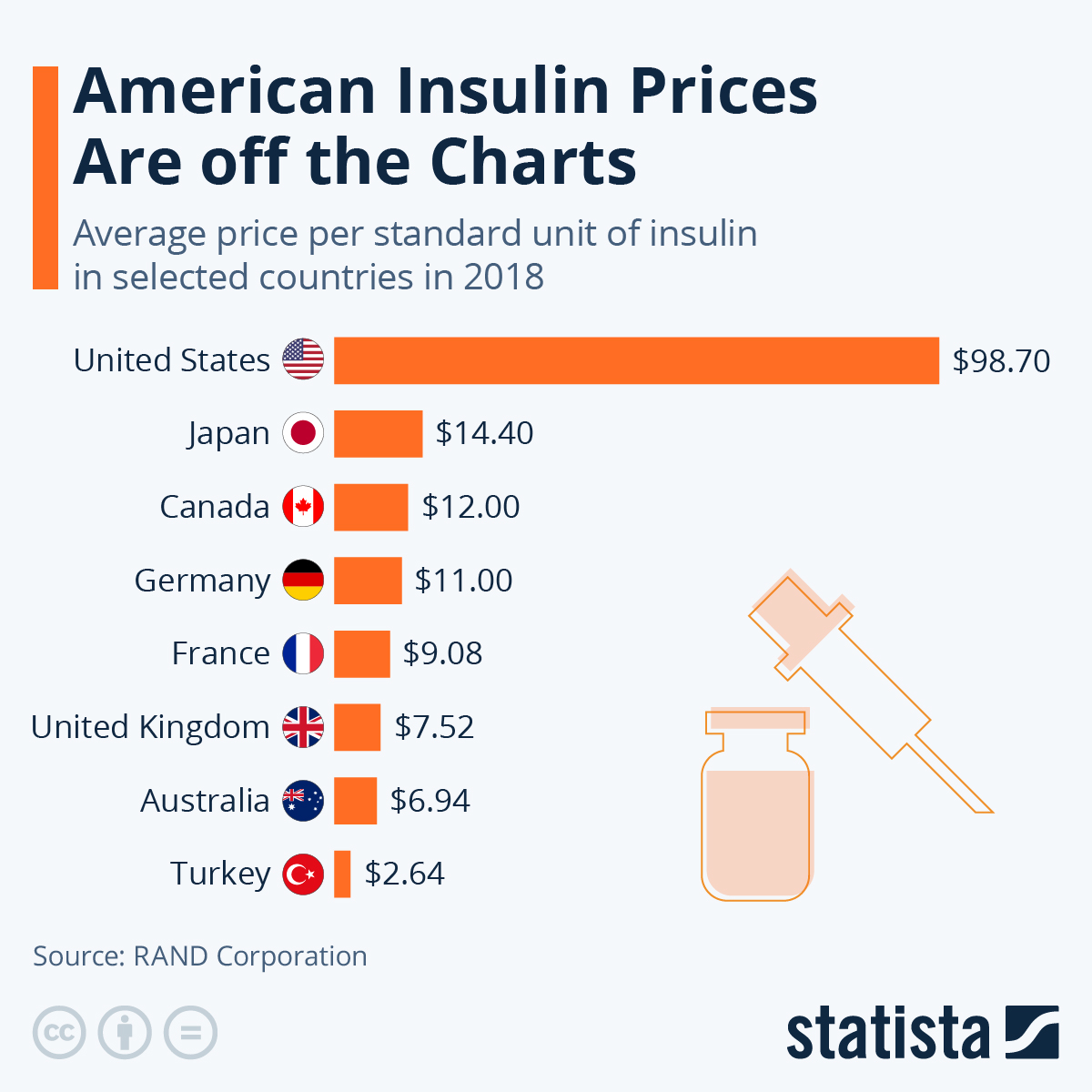

High insulin prices have not earned any U.S. manufacturer many friends, with list prices increasing 54% from 2014 to 2019.

Most troublingly, an estimated 1.3 million uninsured people with diabetes and patients with inadequate insurance have resorted to rationing their insulin. Skipping doses because of high insulin prices has sometimes had tragic and even deadly consequences.

But growing competition has shaken up the insulin market in recent years.

For example, Walmart introduced its own private-brand insulin in 2021. Mylan, a large generic drugmaker, developed a version of long-acting insulin called Semglee, priced 65% lower than its branded competitor. But few consumers use those products.

Efforts to produce cheaper insulin by the nonprofit drugmaker CivicaRx and the state of California are several years out and won’t provide immediate relief.

Then there’s the Inflation Reduction Act, a big spending package Congress approved in 2022. It capped insulin out-of-pocket costs at $35 for Americans with Medicare, a government health insurance program that covers people over 65.

And, in fact, Lilly itself has been trying to disrupt insulin prices. In 2019, the drugmaker introduced insulin lispro, a lower-cost version of its blockbuster insulin, Humalog.

2. What does this mean for Americans who need insulin?

Part of the problem with the existing system is that some patients, especially if they’re uninsured or have high deductibles, end up paying the list price – which can mean spending $1,000 or more a month on insulin. This can be a crushing financial burden.

Lilly’s new $35 out-of-pocket cap means that privately insured patients and those without insurance requiring insulin will spend no more than that monthly for copays. Its 70% reduction in the list price of two popular name brand insulins, Humalog and Humulin, will bring some financial relief. And the company has also reduced its generic lispro’s list price to $25 a vial, down from $126.

The evidence is clear that these price reductions will improve patient adherence – which means fewer missed doses of this lifesaving medication.

3. How might Lilly’s actions affect the whole industry?

Lilly has put pressure on its biggest competitors, Novo Nordisk and Sanofi, to follow suit.

These lower prices could also make Lilly’s insulins affordable to cash-paying patients. As a result, these insulins could be added to the list of drugs provided by pharmacies that are disrupting the U.S. prescription drug industry, like Mark Cuban’s Cost Plus Drug Co. and Blueberry Pharmacy. These companies provide low-cost drugs with transparent markups or through membership programs, typically without insurance.

4. Why did insulin get so expensive in the US?

That lispro, Lilly’s own, cheaper authorized generic insulin, hasn’t completely displaced the equivalent name brand Humalog in the market by now may seem surprising. But it is the result of the complex U.S. prescription drug distribution system.

Insulin prices are the result of a complex set of negotiations between manufacturers and pharmacy benefit managers, which act on behalf of insurers. The three largest – CVS Caremark, Express Scripts and Optum Rx – handle about 80% of all prescriptions.

These middlemen negotiate directly with Lilly and other insulin manufacturers, focusing on two key sums: the list price and the rebate. Manufacturers are paid the list price but then must pay a rebate to the pharmacy benefit managers.

How do pharmacy benefit managers get manufacturers to pay rebates? They maintain formularies – lists of drugs that patients in a health plan can access. If an insulin manufacturer wants to supply diabetes patients, it needs to remain on those formularies. And doing so requires the manufacturer to pay bigger rebates. Otherwise, pharmacy benefit managers can exclude the manufacturer.

In 2016, OptumRx, which negotiates insulin prices for about 28 million people, excluded only four types of insulin from its formulary. By 2022, OptumRx was excluding 13 insulins.

Keeping insulin on formularies, in short, has required high rebates, and list prices have increased along with them. Ironically, as insulin list prices have been rising, manufacturers have been making less money off of insulin sales, while middlemen have been making more.

The key to true price competition is to ensure access to all versions of insulin and to convince patients and providers that people with diabetes can substitute lower-cost versions without compromising their health.

5. What might happen next?

The Federal Trade Commission, a government agency that probes anti-competitive practices, and Congress are now investigating pharmacy benefit managers’ rebate and formulary practices, among other things. These investigations, along with Lilly’s moves, may lead other insulin manufacturers to lower their list prices.

And once its competitors decide whether they will follow Lilly’s example, pharmacy benefit managers will be under a lot of scrutiny to see whether they give preferred formulary placement to the lowest-cost insulin products, or to those that pay the highest rebates.![]()

Dana Goldman, Dean of the Sol Price School of Public Policy; Professor of Pharmacy, Public Policy, and Economics, University of Southern California and Karen Van Nuys, Executive Director of the Value of Life Sciences Innovation program; Fellow at the USC Schaeffer Center, University of Southern California

This article is republished from The Conversation under a Creative Commons license. Read the original article.